Empirical evidence from academic and professional studies, including our own proprietary research, supports the efficacy of this common-sense approach that pairs insider buying with undervaluation.

Tweedy’s new ETFs are distinguished not only by their valuation discipline, informed by decades of the firm’s steadfast adherence to a Benjamin Graham-based, price-driven investment philosophy, but also by their emphasis on coat-tailing the purchase behavior of knowledgeable C-suite executives.

Insider + Value ETFs Commentary, Q1 2026The seemingly indefatigable advance in global equity markets over the last few years faced macroeconomic headwinds in the first quarter of 2026, as global equity markets experienced a decline. Heightened geopolitical tensions, including military conflict involving Iran and the resulting disruption to global oil supply, contributed to increased volatility and a general sense of unease among investors.

The resulting war-related spike in oil prices helped to dampen the very recent outperformance of non-US equities relative to their US counterparts. Nevertheless, the performance of non-US equity markets, as represented by the MSCI EAFE Index, still significantly outperformed US equities for the first quarter and for the 12 months ending March 31.

* Please note that The RBB Fund Trust (the “Trust”) and Tweedy, Browne Company LLC (the “Adviser”), as of 12/31/2025, have entered into an expense limitation agreement under which the Adviser has agreed to reimburse Fund expenses to the extent necessary so that the Fund’s total annual operating expenses (excluding interest, brokerage fees, certain insurance costs, and extraordinary and other non-routine expenses) through the period ending December 31, 2027 do not exceed 0.80% of the Fund’s average daily net assets, and also will terminate automatically upon the expiration or termination of the Fund’s advisory contract with the Adviser.

Total Returns are shown net of fund management and operating expenses. The MSCI World Index (in USD) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI EAFE Index (in USD) is an unmanaged, free float-adjusted capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the US and Canada. The MSCI EAFE Index (USD) reflects the return of the MSCI EAFE Index for a US dollar investor.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and the value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The current performance of the Fund may be lower or higher than the performance quoted. For performance data that is current to the most recent month end, click here (COPY) and here (ICPY) or call 1-800-617-0004.

Shares are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. The market price returns are based on the official closing price of an ETF share or, if the official closing price isn’t available, the midpoint between the national best bid and national best offer (“NBBO”) as of the time the ETF calculates current NAV per share. NAVs are calculated using prices as of 4:00 p.m. Eastern time.

As we write in mid-April, a cease-fire in the Iranian conflict has helped to spark a rebound in global equity indices, led by an unusually robust rally in US-based high technology companies. It remains to be seen whether market sentiment will revert to the AI-related market concerns that had emerged prior to the outbreak of hostilities.

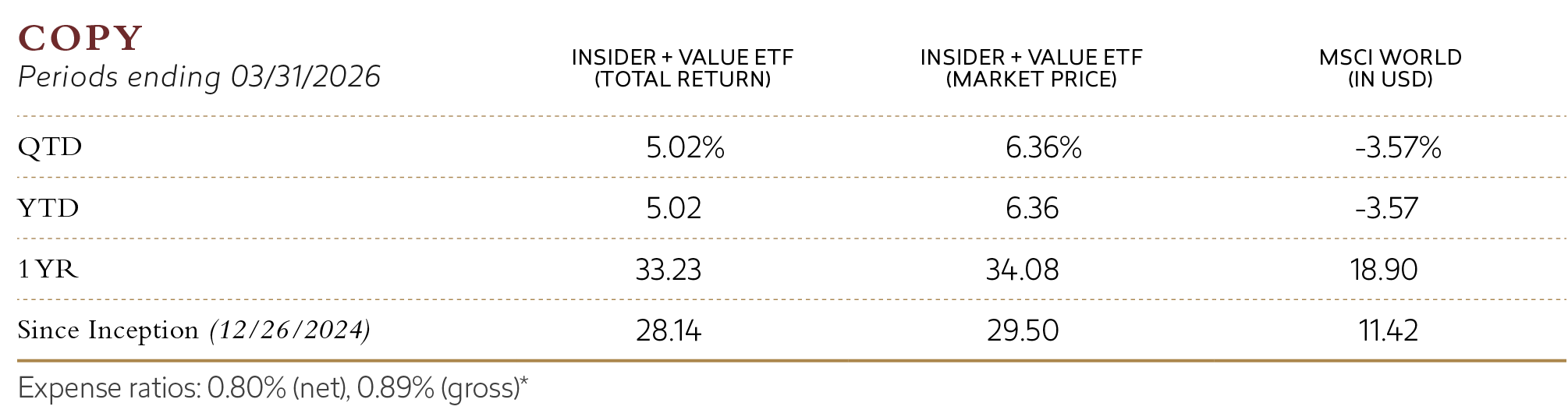

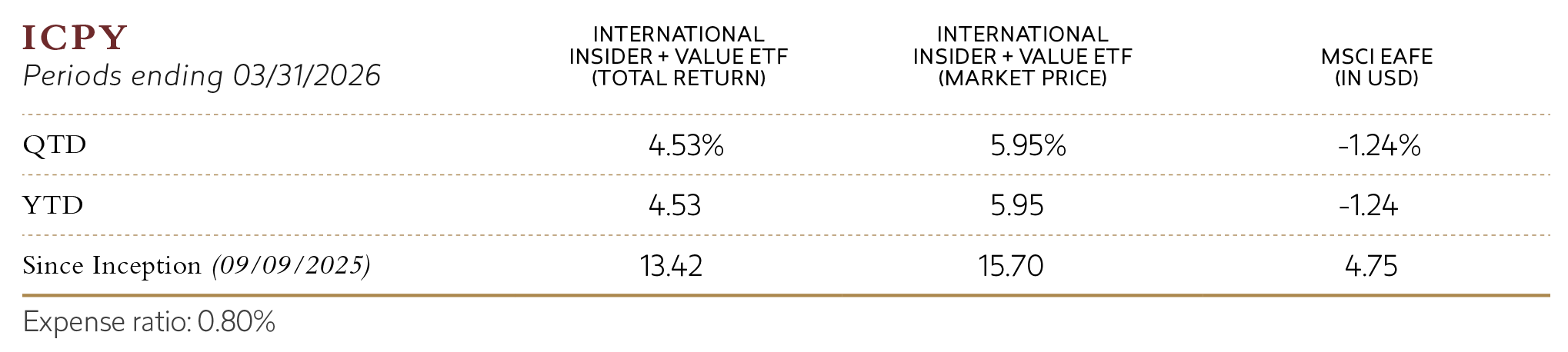

Against this uncertain backdrop, the results of the Tweedy, Browne Insider + Value ETFs have remained encouraging. The Tweedy, Browne Insider + Value ETF (COPY) returned 6.36% during the quarter, compared with -3.57% for the MSCI World Index (in USD). The Tweedy, Browne International Insider + Value ETF (ICPY) returned 5.95%, versus -1.24% for the MSCI EAFE Index (in USD). Given that both ETFs now fully hedge non-U.S. currency exposure, currency-hedged benchmarks may provide a more comparable reference point. On that basis, the MSCI World Index (Hedged to USD) returned -2.96%, and the MSCI EAFE Index (Hedged to USD) returned 0.85% during the same period.

While it is still early days in their development, the performance of COPY and ICPY has been quite reassuring. Since their respective inceptions in December of 2024 and September of 2025, through April 20, 2026, COPY and ICPY have generated cumulative returns of 45.43% and 19.77%, producing 1,908 basis points1 and 545 basis points of excess return, respectively, over and above their primary benchmarks. Investor interest has continued to build alongside these good returns, and as of quarter-end, COPY had grown to approximately $286 million in assets, while ICPY had reached roughly $59 million.

Empirical evidence from academic and professional studies, including our own proprietary research, supports the efficacy of this common-sense approach that pairs insider buying with undervaluation.

Tweedy’s new ETFs are distinguished not only by their valuation discipline, informed by decades of the firm’s steadfast adherence to a Benjamin Graham-based, price-driven investment philosophy, but also by their emphasis on coat-tailing the purchase behavior of knowledgeable C-suite executives. These are corporate insiders who are buying shares in their own companies or returning capital to shareholders through meaningful share buybacks. When paired with our proprietary multi-factor value model, this insider-focused lens has enabled us to build a portfolio of fundamentally sound and undervalued businesses with management teams that think like owners—in our view, a rare yet valuable combination.

This focus on insider purchase behavior also helps us capitalize on what we refer to as the “insider’s edge,” i.e., the unique insights that senior executives and informed directors can have regarding the prospects for improvement in their company’s condition, and ultimately, its share price. Empirical evidence from academic and professional studies, including our own proprietary research, supports the efficacy of this common-sense approach that pairs insider buying with undervaluation. COPY, which launched at the end of 2024, applies this approach globally, while ICPY, launched in September 2025, focuses primarily on non-US companies.

At the sector level, Energy was by far the largest contributor across both ETFs. Consumer Staples and Information Technology also contributed meaningfully, while Materials, Financials, and Utilities added positively as well. Consumer Discretionary was the largest detractor in both ETFs. Communication Services detracted on balance, while Health Care was mixed, detracting in COPY but contributing modestly in ICPY. Industrials were positive overall, although their contribution was more modest than that of the leading sectors.

In terms of their industry exposures, the largest positive contributions came from oil & gas, energy equipment & services, metals & mining, banks, food products, and technology hardware. In ICPY, insurance and semiconductor equipment also contributed meaningfully. The principal industry detractors were financial services, automobiles, media, containers & packaging, apparel & luxury goods, and passenger airlines. Specialty retail and construction materials also detracted.

From a geographic perspective, contributions were led by Canada, South Korea, Singapore, Spain, Hungary, and Austria, with U.S. holdings also contributing meaningfully in COPY. The largest country-level detractors were Italy, France, Sweden, Hong Kong, and Germany.

Among individual holdings, notable contributors in COPY included Noble Corp, Repsol, Cenovus Energy, DPM Metals, StoneX Group, Tidewater, and Samsung Electronics. In ICPY, Repsol, Cenovus Energy, Beazley, Samsung Electronics, DPM Metals, First Resources, and Hafnia were among the larger contributors. On the negative side, BFF Bank was the largest detractor in both ETFs. Other meaningful detractors included OSB Group, Norion Bank, Volvo Car, Jet2, Burberry, Télévision Française, HCI Group, and Cleveland-Cliffs.

From a market capitalization standpoint, the strongest contributions came from the portfolio’s largest companies with small caps acting as an overall drag in both ETFs.

Currency impact on our ETF portfolios during the quarter was mixed. The U.S. dollar weakened against several developed market currencies, including the Swedish krona and Canadian dollar, and strengthened against a number of Asian currencies, most notably the Japanese yen and South Korean won. Both ETFs began fully hedging foreign currency exposure late last year, consistent with the strategy’s original design. We view currency fluctuations as an uncompensated source of volatility and expect the funds to remain fully hedged going forward, allowing underlying business performance to drive results.

Heightened market volatility during the quarter helped to spark an increase in insider buying activity. Both ETFs initiated and added to positions where insider buying and share price weakness created more attractive entry points, while trimming or exiting holdings where valuations became less compelling or capital could be redeployed more effectively.

The examples below should provide some insight into the types of opportunities we uncovered during the quarter:

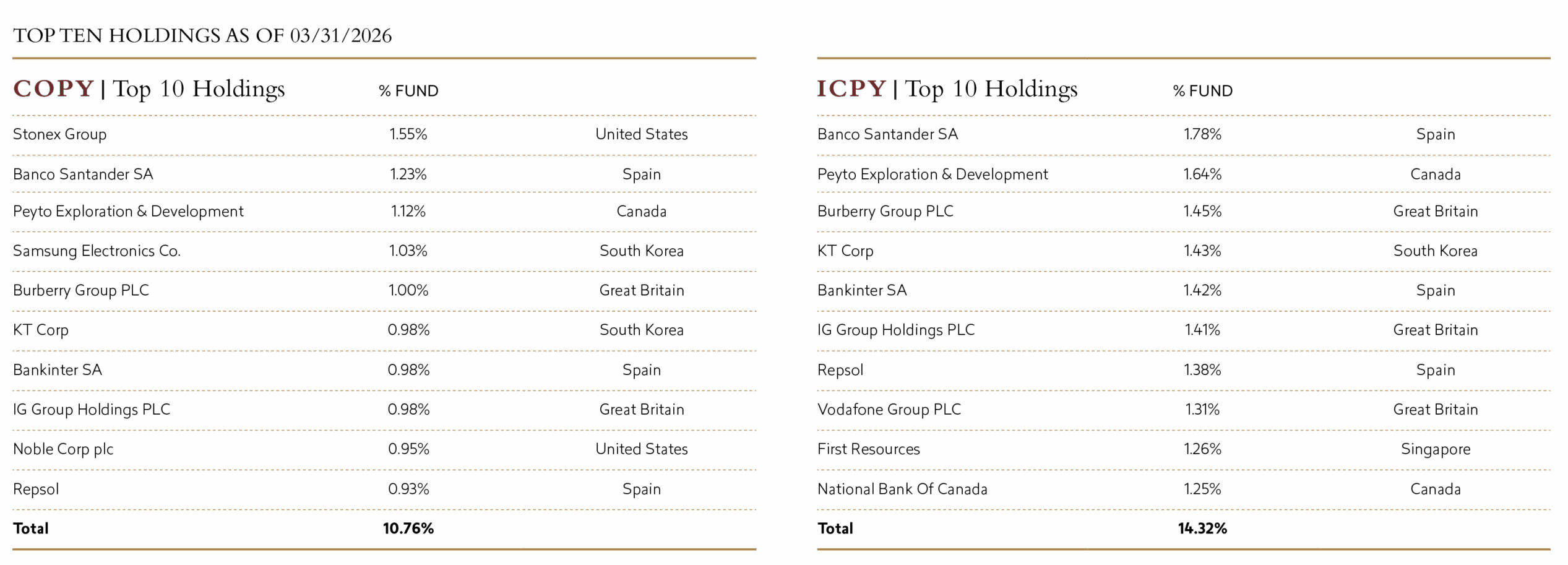

For more portfolio information as of 03/31/2026, check out Insider + Value ETF Factsheet (COPY) and International Insider + Value ETF Factsheet (ICPY).

We have been encouraged over the last year by the nascent resurgence in value-oriented equities, particularly smaller and medium capitalization non-U.S. equities where informed corporate insiders have been meaningful buyers of their company’s shares. Prior to the outbreak of hostilities in late February, the proverbial “puck,” to borrow from Wayne Gretzky, genuinely appeared to be coming to where we had “skated,” reflecting in our view a long overdue sea change in equity market leadership. However, since the outbreak of hostilities in Iran, relative momentum in equity markets has once again, at least in the very near term, gravitated toward U.S. based technology stocks. Despite this war-induced rotation, we remain hopeful that the fundamental conditions that underpinned the earlier change in market sentiment remain largely in place, and continue to point to a more promising long-term opportunity set for patient, value-oriented investors.

While we cannot know for sure, we suspect that given these cross currents of concern, the recent surge in market volatility may not yet have run its course. In such an unsettling environment, we are reassured by our ETF portfolios’ attractive valuations, and the invaluable signals we receive from the behavior of knowledgeable corporate insiders.

We are grateful for your interest in our new ETFs, and thank you for your continued trust and confidence.

Roger R. de Bree, Andrew Ewert, Frank H. Hawrylak, Jay Hill, Thomas H. Shrager, John D. Spears, Robert Q. Wyckoff, Jr. | Investment Committee | Tweedy, Browne Company LLC

April 2026

This material must be preceded or accompanied by a prospectus. An investor should consider the investment objectives, risks, and charges and expenses of the fund carefully before investing. Click here or call 1-800-617-0004 for a copy of the Fund’s prospectus, which contains this and other information about the fund. The prospectus should be read carefully before investing.

All investing involves the risk of loss, including the loss of principal. The Fund’s buyback strategy is based, in part, on the premise that stocks of companies that engage in share buyback purchases are often anticipated to perform well because they typically are a signal that a company’s management believes its shares are undervalued. This positive signal from management may cause the value of such shares to rise. There is no certainty that management of a company undertook a buyback strategy because it believes its stock is undervalued; a company could be using buybacks to increase their price to earnings or other ratios, to alleviate excessive dilution, as a defensive measure, or to cut their own capital expenditures, thereby potentially limiting future growth.

To implement its investment strategy, the Adviser may require access to large amounts of financial data and other data supplied by various data providers. The inability to access large amounts of financial and other data from data providers could adversely affect the Adviser’s ability to use quantitative methods to select investments.

International investing may be subject to special risks, including, but not limited to, currency exchange rate volatility, political, social or economic instability, less publicly available information, less stringent investor protections, and differences in taxation, auditing and other financial practices. Investment in emerging market securities involves greater risk than that associated with investment in securities of issuers in developed foreign countries. These risks include volatile currency exchange rates, periods of high inflation, increased risk of default, greater social, economic and political uncertainty and instability, less governmental supervision and regulation of securities markets, weaker auditing and financial reporting standards, lack of liquidity in the markets, and the significantly smaller market capitalizations of emerging market issuers.

The Fund may invest in derivative instruments, including forward currency exchange contracts, which may be leveraged and may result in losses. Investments in derivative instruments may result in losses exceeding the amounts invested. The Fund’s practice of hedging exposure to foreign currencies where practicable, tends to make the Fund underperform a similar unhedged portfolio when the dollar is losing value against the local currencies in which the Fund’s investments are denominated.

Value investing involves buying stocks that are out of favor and/or viewed as undervalued by the Adviser in comparison to their peers or their prospects for growth. Securities of companies with micro-, small- and mid-size capitalizations tend to be riskier than securities of companies with large capitalizations. This is because micro-, small- and mid-cap companies typically have smaller product lines and less access to liquidity than large cap companies, and are therefore more sensitive to economic downturns.

ETFs are subject to additional risks that do not apply to conventional mutual funds, including the risks that the market price of an ETF’s shares may trade at a premium or discount to its net asset value, an active secondary trading market may not develop or be maintained, or trading may be halted by the exchange in which they trade, which may impact an ETF’s ability to sell its shares. Shares of any ETF are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns.

Holdings are subject to change and risk.

DEFINITIONS

The Tweedy, Browne Insider + Value ETF and Tweedy, Browne International Insider + Value ETF are distributed by Quasar Distributors, LLC.