There is only one logical reason for corporate insiders to reach into their wallets and make free-will, open-market purchases—they believe the stock price will increase.

We believe this quarter’s results reflect the merit of our approach: a valuation-sensitive, bottom-up portfolio… strengthened by the signaling power of material insider commitment.

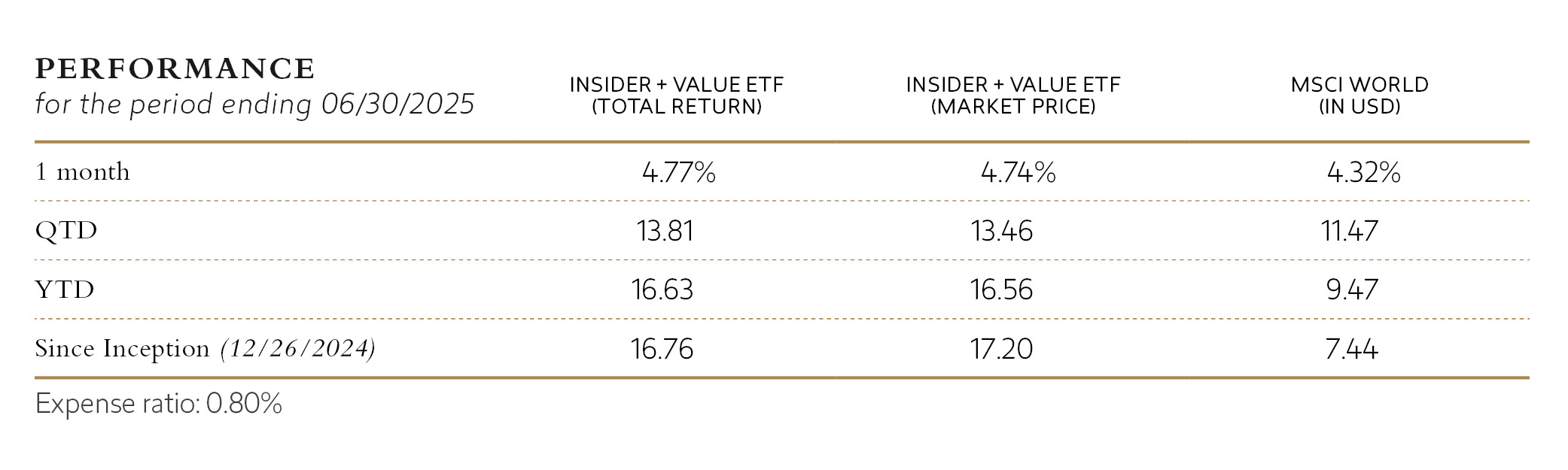

ETF Commentary, Q2 2025While it is still early days for the Tweedy Browne Insider + Value ETF (NYSE ticker: COPY), the Fund is off to an excellent start, producing very good absolute and relative returns for the second quarter, year-to-date, and since inception measurement periods.

Launched on December 26 – just days shy of year-end – COPY finished the second quarter up 13.46%, comfortably outpacing the 11.47% return of the MSCI World Index (in USD) (the “benchmark”). Year-to-date through June 30, the Fund is up 16.56% versus 9.47% for its benchmark. As of our writing, the Fund is up 19.24% since inception through July 11, more than doubling the 8.67% return of its benchmark. COPY produced these encouraging returns, despite a market environment that has been relatively volatile and heavily tilted toward a narrow set of high-multiple growth stocks.

Tweedy’s new ETF is distinguished not only by its valuation discipline, informed by decades of steadfast adherence to a Benjamin Graham-based, price-driven investment philosophy, but also by its emphasis on coat-tailing the purchase behavior of knowledgeable C-suite executives. These are corporate insiders who are buying shares in their own companies or returning capital to shareholders through meaningful share buybacks. When paired with our proprietary multi-factor value model, this insider-focused lens has enabled us to build a portfolio of fundamentally sound and undervalued businesses with management teams that think like owners—in our view, a rare yet valuable combination.

This focus on insider purchase behavior also helps us capitalize on what we refer to as the “insider’s edge,” i.e., the unique insights that senior executives and informed directors can have regarding the prospects for improvement in their company’s condition, and ultimately, its share price. Empirical evidence from academic and professional studies, including our own proprietary research, supports the efficacy of this common-sense approach that pairs insider buying with undervaluation.

While COPY’s investment approach is largely quantitative and factor-driven, combining insider purchase data and value-oriented statistical metrics to identify investment candidates across multiple geographies and market capitalizations, the research process does employ a light qualitative review to ensure data integrity. This review helps ensure that insider purchases were free-will (voluntary) purchases, and that there were no overarching issues that our model may have failed to address.

There is only one logical reason for corporate insiders to reach into their wallets and make free-will, open-market purchases—they believe the stock price will increase.

The valuation gap between popular growth stocks and more attractively priced value-oriented non-U.S. enterprises remains significant.

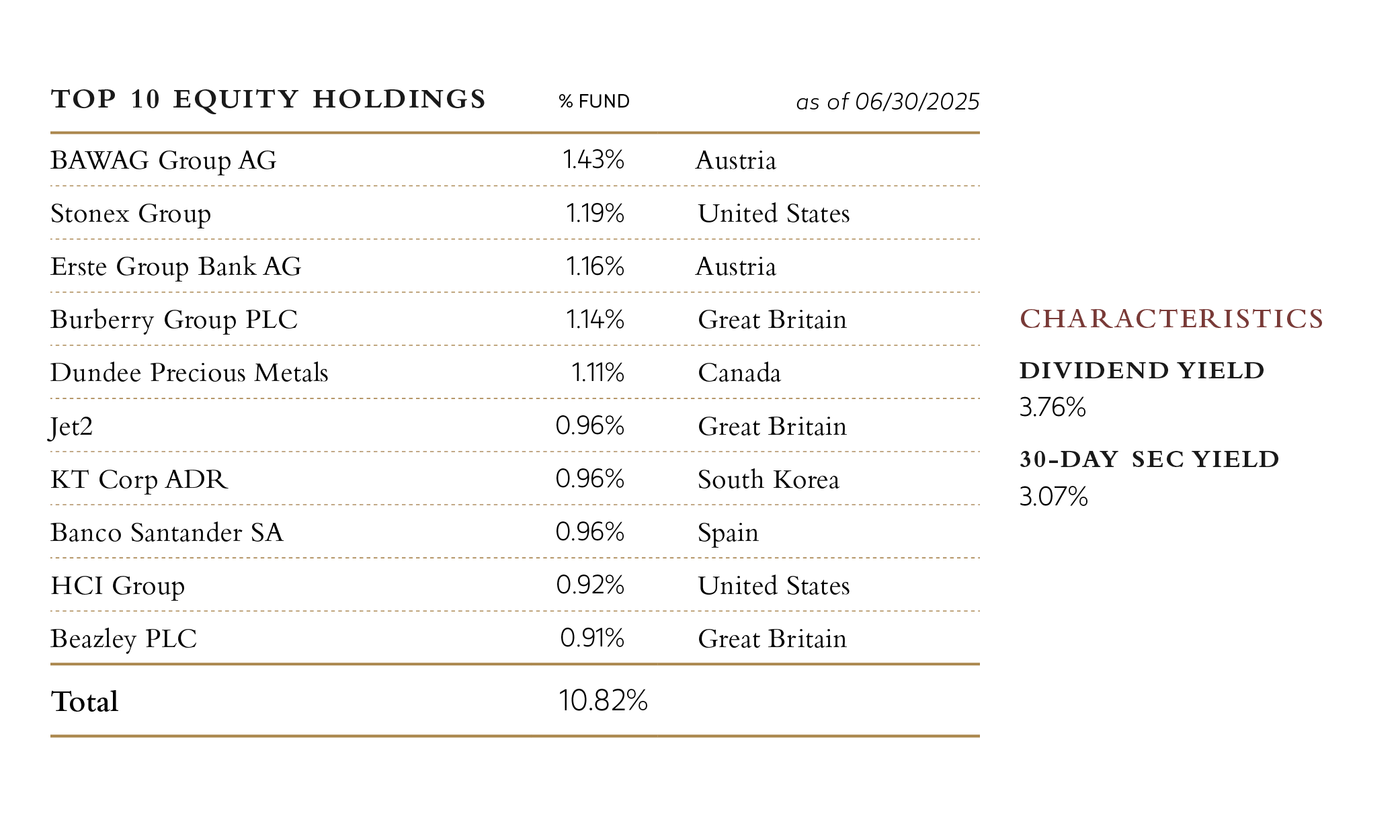

As of June 30, COPY was broadly diversified by issue, country, industry, and market capitalization. The portfolio consisted of equity securities from the United States, Europe, the United Kingdom, and across Asia, and it included the more developed of the emerging markets. While the Fund has benefited from this diversified posture, it bears little resemblance to its benchmark index. Its country, industry, and market capitalization exposures vary considerably from those of the benchmark.

As of June 30, the Fund was invested in 179 individual equities across 22 countries, including the U.S. These holdings spanned 10 sectors, and 48 industries, as classified by GICS. The largest country allocations were the U.S. (26.91%), the UK (14.62%), and Canada (10.84%), followed by Germany (8.04%), South Korea (6.5%), and France (5.62%).

From a sector standpoint, the Fund’s largest weightings were in Financials (29.44%), Consumer Discretionary (14.77%), and Industrials (11.73%). Notable industry weightings included banks (15.18%), oil & gas (10.20%), insurance (5.49%), capital markets (5.20%), metals & mining (3.29%), chemicals (3.15%), and automobile components (3.12%).

While market capitalizations will vary over time, the Fund currently skews toward small- and mid-cap companies, with 79% of the equity holdings having market capitalizations of $25 billion or less.

As of quarter-end, the Fund had a weighted average price-to-earnings ratio of 13.2X, an average annual dividend yield of 3.76%, an active share of 97.30%, and assets under management totaling $72.9 million.

For more portfolio characteristics, check out the Insider + Value ETF Factsheet (06/30/2025).

Performance during the quarter was broad-based, reflecting the global scope and diversification of the portfolio. From a geographic standpoint, Britain led contributions, driven by the Fund’s holdings in financials, retail, and specialty manufacturing. South Korea followed, where undervalued financials such as Hana Financial Group and KB Financial rallied meaningfully, bolstered by favorable interest rate dynamics and solid loan growth. Canada was another bright spot, helped by select positions in banks and materials stocks.

At the sector level, financials once again took center stage. Strong results from banks and capital markets firms across multiple regions helped drive returns. Consumer discretionary names also added meaningfully, buoyed by improving sentiment in retail and travel. Industrials followed close behind, supported by demand in components, logistics, and machinery.

Looking more granularly, banks, specialty retailers, and semiconductor suppliers were among the strongest industry contributors. Several mid-sized companies stood out—particularly those with market caps between $2 billion and $10 billion—underscoring our long-held belief that opportunity often lies in the less trafficked areas of the market.

There were a few modest detractors. Health care, especially pharmaceuticals and medical equipment firms, lagged, held back by concerns over potential government intervention in drug pricing and by tariff uncertainty. Energy also detracted, with oil price volatility and cautious forward guidance weighing on results.

The U.S. dollar’s weakness during the quarter provided a tailwind to Fund performance, amplifying local currency returns when translated back into U.S. dollars. This included currency-related gains in our euro, pound sterling, and several Asia-Pacific holdings. Over time, it is our intention to hedge the Fund’s foreign currency exposure back into the U.S. dollar. Going forward, then, it is likely that the Fund’s returns will not benefit when the U.S. dollar weakens. Conversely, it should be at least partially hedged against the adverse impact of a strengthening U.S. dollar on foreign currency returns. Over the long term, both empirical data and our own experience suggest that exposure to highly volatile foreign currencies offers little, if any, meaningful advantage.

Overall, we believe this quarter’s results reflect the merit of our approach: a valuation-sensitive, bottom-up portfolio grounded in factor-based business fundamentals, diversified across geographies and industries, and strengthened by the signaling power of material insider commitment.

While the second quarter was a relatively quiet period for new insider buys, we were able to deploy capital into a variety of companies that offered an appealing mix of quality, value, and management alignment.

Notably, we initiated a position in UnitedHealth Group after the shares declined sharply early in the quarter triggered by future earnings and cost warnings, executive suite turmoil, and reports that the DOJ was probing the company’s billing practices. Shortly after the price declines in mid-May, there was a cluster of insider buys in UnitedHealth stock initiated by a number of the company’s C-suite executives and directors. Stephen Hemsley, the company’s Chairman, and John Rex, the company’s CFO purchased $25 million and $5 million worth of shares, respectively. In addition, two directors, Timothy Flynn and John Noseworthy, bought shares worth $492,000 and $94,000, respectively, around the same time. At the time of COPY’s purchase, the shares were priced near what the insiders had paid, and according to our proprietary valuation model were undervalued, trading at roughly 11 times trailing earnings, and a little over 9 times enterprise value to EBITA (earnings before interest, taxes and amortization). While the company remains under a cloud of government scrutiny, it remains one of the most competitively advantaged health care businesses globally, with attractive economics and a long runway for potential future growth, something apparently not lost on the insiders.

Elsewhere, we established new positions in GQG Partners, Stabilus, and SKF. Each of these companies operates in essential, cyclical industries—asset management, motion control systems, and industrial bearings, respectively—and, at or around the ETF’s purchase, were trading at attractive valuations, had rock-solid balance sheets, and had insiders making voluntary purchases of the company’s shares at or around the prices the ETF paid. Insider buys included $4.32 million in purchases of GQG stock by Rajiv Jain, the company’s Chairman and CIO; $110,000 worth of shares in Stabilus purchased by the company’s Chairman, Stephen Kessel; and $18.02 million worth of shares purchased in SKF by Vice Chair Hakan Buskhe.

Other additions to COPY’s portfolio where insiders were active included Watches of Switzerland (Chairman Ian Carter: $125,000 buy), the Danish shipping firm TORM (CEO Jacob Meldgaard: $440,000 buy), and Buzzi Unicem, an Italian cement producer (CEO Pietro Buzzi: $7.18 million buy). In all cases, our purchases were informed by both an attractive valuation and material, free-will purchases by key C-suite executives, and/or knowledgeable directors—tangible signs that key members of management believed in the value of their own businesses.

On the sales side, we trimmed or exited several positions where valuations had approached our estimates of intrinsic value or where fundamental progress had stalled. These included FS KKR Capital, Capri Holdings, and Securitas. As always, we reallocated capital to names with more attractive valuations, better return potential, and more immediate insider buying.

Looking ahead, we recognize that the global investment landscape remains exceedingly complex. While equity markets gained considerable momentum in the second quarter, volatility also picked up, sparked by concerns over tariffs, rising government debt and deficits, ongoing wars, escalating geopolitical tensions, and their potential implications for inflation, interest rates, and ultimately, corporate earnings. While we remain cautious amid elevated and climbing valuation multiples, we are encouraged by the relative discounts afforded investors in non-U.S. equity markets, particularly in small- and mid-cap companies where knowledgeable corporate insiders have been actively buying shares. In our view, the valuation gap between popular growth stocks and more attractively priced value-oriented smaller and medium-sized non-U.S. enterprises remains significant. It presents a meaningful opportunity for disciplined, price-sensitive investors.

We thank you for your continued trust and confidence.

Roger R. de Bree, Andrew Ewert, Frank H. Hawrylak, Jay Hill, Thomas H. Shrager, John D. Spears, Robert Q. Wyckoff, Jr. | Investment Committee | Tweedy, Browne Company LLC

July 2025